Dental Insurance Coverage

Reader-supported. We may earn a commission from links on this page. Advertising disclosure.

In this article

Dental insurance can lower what you pay for care, but it does not work like medical insurance. Plans use categories, limits, and networks that shape what’s covered and what you owe, which is why surprises happen even when you think you’re “covered.”

This guide explains how dental insurance typically works so you can plan care, compare options, and avoid unexpected bills.

What Does Dental Insurance Cover?

Most dental plans group benefits into three buckets: preventive, basic, and major. This is to outline what the plan will cover.

These labels guide cost-sharing and limits, but the details depend on your specific policy and network rules. Before scheduling care, check how your plan defines each category and what conditions apply.

Preventive Services

Preventive care focuses on identifying issues early and maintaining oral health, which is why plans often prioritize it. Coverage commonly includes:

- Exams

- Cleanings

- Routine imaging

- Fluoride treatments (often limited by age and plan)

- Sealants (often limited to specific age groups)

Calculate your dental savings now with a DentalPlans plan. Visit DentalPlans.

Keep in mind that frequency limits usually apply. Even when preventive care is well covered, plans may cap how often you can receive each service within a benefit year, so timing matters.

If you’re due for routine care, confirm how many visits your plan allows this year before you book.

Basic Services

Basic services typically cover common repair needs that come up between checkups. This category often includes:

- Fillings

- Simple extractions

- Certain emergency visits

Because definitions vary, the same procedure can be classified as basic on one plan and major on another. When a dentist recommends treatment, ask how your plan classifies it so you can estimate your share.

Major Services

Major services usually involve more complex or costly care, such as:

- Crowns

- Bridges

- Dentures

- Implants (may be limited or excluded, depending on the plan)

- Periodontal treatment (coverage and classification vary by plan)

- Some oral surgery

Plans often impose higher cost-sharing, waiting periods, and annual caps on these services, shifting more costs to you. Coverage can also depend on whether the procedure replaces an existing restoration or treats a new problem.

Before starting major work, request a written pre-treatment estimate to understand how the benefits apply.

Common Limits and Exclusions in Dental Insurance

If dental insurance feels frustrating, it’s often because of limits and exclusions rather than the procedure list itself. These rules govern timing, frequency, and eligibility and explain many denied or reduced claims. Understanding them upfront can save you time, money, and stress.

Here are the limits that most often surprise people:

- Waiting periods — Delays before coverage starts for certain basic or major services.

- Frequency limits — Caps on how often the plan will pay for exams, cleanings, or imaging.

- Preexisting clauses — Some plans have limits for conditions that existed before you enrolled, including limits on replacing teeth that were already missing.

- Annual maximums — A yearly dollar cap on what the plan will pay toward your care.

If you’re dealing with pain, swelling, or signs of infection, don’t delay care while you sort out benefits. For non-urgent treatment, call your insurer or check your member portal to confirm how these rules apply to you.> Tired of paying full price for dental work? Save with Discount Dental Plans. Learn more here or call [(833) 704-2246](tel:(833) 704-2246)

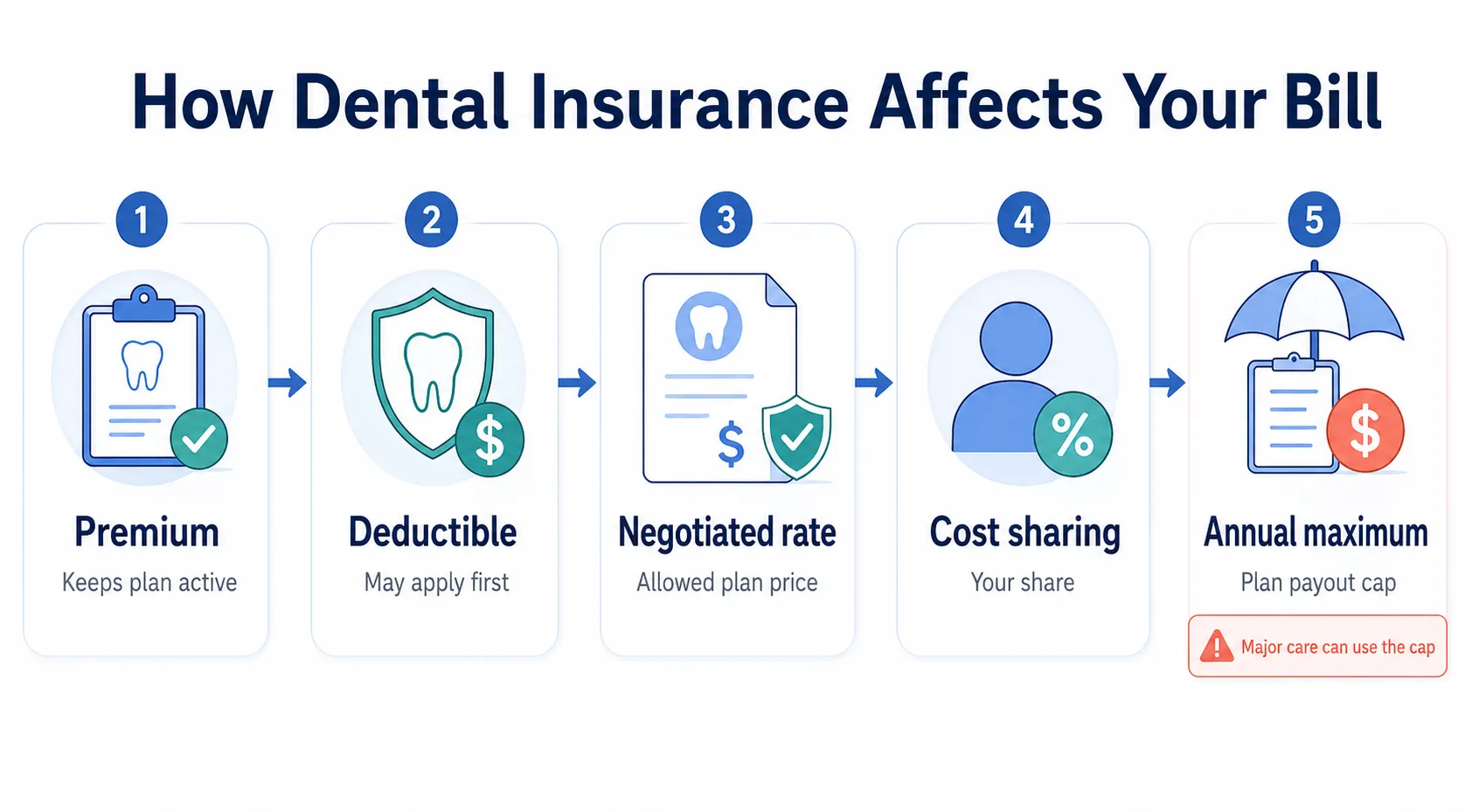

Understand Your Costs Under Dental Insurance

What you pay for dental care depends on several moving parts, not just a coverage percentage.

Premiums, deductibles, negotiated rates, and cost sharing all interact, which is why two people with the same procedure can owe very different amounts. Knowing the cost math ahead of time helps you budget and avoid surprises.

Premiums

Your premium is the monthly amount you pay to keep the plan active, whether you use dental services that month or not.

Plans with lower premiums often trade off with higher deductibles, narrower networks, or lower annual maximums. Looking at premiums alone can be misleading if you expect to need more than routine care.

Before enrolling, compare the premium alongside expected treatment needs for the year.

Cost Sharing

Cost sharing is your portion of the allowed cost for a service after any deductible applies. Plans may use copays, which are set dollar amounts, or coinsurance. These are a percentage of the plan’s allowed rate and may vary by service category.

Because insurers calculate benefits from negotiated rates, your dentist’s list price is not always the number that matters. Ask whether a service uses a copay or coinsurance so you can estimate your out-of-pocket share.

Annual Maximums

Most dental plans have an annual maximum, which is the total amount the plan will pay in a benefit year. Once you reach that cap, you’re responsible for the full cost of additional care until the next benefit year begins.

Major procedures can quickly consume a large portion of the maximum, especially when combined with higher cost-sharing. If you anticipate major treatment, confirm your remaining annual maximum before you schedule.

Different Types of Dental Insurance Plans

Plan type affects your choice of dentist, costs, and the predictability of your bills. Understanding the main designs helps you match a plan to your preferences and care needs without overpaying.

PPO Plans

Dental PPO plans usually offer the most flexibility in choosing a dentist. You can see out-of-network providers, but you’ll typically pay less when you stay in-network because of discounted rates. This option often works well if you already have a preferred dentist.

Check whether your dentist participates in the PPO network before enrolling.

Dental HMOs

Dental HMOs often emphasize lower premiums and predictable copays. You generally choose a primary dentist within the network, and referrals may be required for specialty care. The tradeoff is less flexibility if you want to see a provider outside the network.

Other Types

Some plans fall between PPOs and HMOs, such as EPO or POS designs, while others operate as fee-for-service or discount arrangements. Each has its own rules around networks, referrals, and pricing, which can affect total cost.

Reading the plan summary closely helps you spot these differences. If a plan type is unfamiliar, ask the insurer to explain how claims and payments work.> Get the dental care you need at a price you can afford. Find your DentalPlans savings now.

How to Compare and Choose Dental Plans

Choosing a dental plan is easier when you focus on fit rather than brand names. A short checklist can help determine whether a plan meets your care needs and fits your budget for the year ahead.

Here are the questions that matter most:

- Network size — Are your preferred dentists in-network, and how easy is it to switch providers?

- Waiting periods — Are there delays before basic or major services are covered?

- Annual maximum — Is the cap realistic for the care you expect this year?

- Exclusions — Are cosmetic care, orthodontics, or replacement timelines limited?

If an insurer can’t give clear answers in writing, slow down and compare another option.

What to Ask the Insurance Provider

When reviewing a plan, request a summary of benefits and any exclusions. Clarify how the plan defines preventive, basic, and major services, and whether pre-treatment estimates are available for major work. These details matter more than marketing language.

Before You Book

Before starting major treatment, request a written pre-treatment estimate from your dentist or insurer. This estimate shows how the plan expects to pay and what you’re likely to owe, based on current benefits. It’s one of the best ways to prevent billing surprises.

Dental insurance works best when you confirm details before care begins. Reviewing your benefits, staying in-network, and scheduling treatment in line with plan rules can reduce stress and costs.

Start with a benefit check and a written pre-treatment estimate for any major procedure, and use what you learn to choose care with confidence.

Sources

- American Dental Association. “Typical dental plan benefits and limitations.” ADA.org, 2023.

- American Dental Association. “Introduction to dental benefits.” ADA.org, 2022.

- American Dental Association. “Dental insurance 101: PPO plan basics.” ADA.org, 2022.

- National Association of Insurance Commissioners. “Understanding your dental insurance: Cavities vs cosmetic care.” NAIC Consumer Insight, 2023.

- HealthCare.gov. “Dental coverage in the Marketplace.” HealthCare.gov, 2024.

- HealthCare.gov. “Dental plan information and glossary.” HealthCare.gov, 2024.

- Centers for Medicare & Medicaid Services. “Dental services.” CMS.gov, 2024.

- Medicare.gov. “Dental services coverage.” Medicare.gov, 2024.

- National Association of Dental Plans. “Understanding dental benefits.” NADP.org, 2023.

- American Dental Association News. “Annual maximums and dental benefits.” ADA News, 2025.

UCLA-trained dentist practicing in public health. Focuses on whole-body approach to dental care.

Experienced dental health writer dedicated to providing accurate, accessible information.

Related Articles

How To Find Affordable Dental Insurance & Alternative Options

Discover ways to cut back on your out-of-pocket expenses when visiting the dentist, including affordable dental insuranc...

Which Insurance Options are Best for Major Dental Work?

Top Dental Insurance Plans for Major Dental Work Most dental insurance plans cover preventive dental services like annua...

Best Dental Insurance for Kids

A child's oral health correlates with their quality of life and overall health. Common dental issues, like cavities, can...

Does Medicare Provide Dental Coverage?

Wondering how to get dental coverage with Medicare? We explain everything you need to know about Medicare dental insuran...